Summary of day one of the BAFM.

The second day of the 7th BAFM – Building African Financial Markets seminar continued with more explanations on changes in the global scene and how they could affect African exchanges.

Michele Carlsson of Nasdaq said immediate top compliance concerns were the need to fully understanding regulations and how they affect exchanges, and the inability of technology to meet current market requirements. She said it was important for exchanges to have market surveillance systems that could look at several assets classes, do powerful visualizations, have flexible alerting, and enable real-time controls as well as being scalable and resilient.

Anne Clayton of the Johannesburg Stock Exchange spoke on the impact that various new European Union regulations that could have on African capital markets. These include rules on general data protection (GDPR, May 2018), benchmark regulation (BMR – Jan 2018), financial instruments regulations (MiFID II – Jan 2018) and others on derivatives trading. She explained that data on GDPR, EU citizens had to be notified of data breaches and they also the right to be forgotten if they requested it i.e. to have all their data wiped out from a system – .but that is in conflict with “know your customer” (KYC) and “anti-money laundering” (AML) laws, which require that financial data, is kept for seven years. African exchanges have low liquidity and the costs of compliance keep going up, now estimated at 5-10% of turnover, even where there is no uptake of products or use of some of the new rules. Many of them have low liquidity and are heavily dependent on foreign investors to provide liquidity, but such investors are sensitive to any policy or taxes which can make them shift to other markets. But non-compliance could result in heavy penalties for companies.

Dr. Anthony Miller spoke of new opportunities from linking exchanges to the United Nations Sustainable Development Goals (SDGs) through new products. Last week Fiji launched a green bond at the London Stock Exchange while there was a gender bond floated in Asia to support women funded entrepreneurs. This is at a time that companies like Bloomberg are tracking the growth of green funds around the world, while many other investors are eliminating carbon investments, like coal, from their portfolios.

Block chain and bitcoin were top topics of discussion on day two of the BAFM. One talk was an explanation on the different aspects of block chain technology, which could offer African institutions the ability for Africa to leapfrog old hurdles. Sofie Blakstad spoke of using block chain to provide cheaper rural financing that is much cheaper than from commercial banks, and that the technology also enabled an unprecedented level of validation of the impacts of targeted funding programs such as micro-finance institutions e.g. how ethical or green their funding programs are, by looking at data from the beneficiaries.

(Away from the BAFM, on the same day, Juliani, a popular Kenyan gospel musician launched Juliani “Hela” a loyalty point-based currency earned by customers on every purchase of an official Juliani event ticket, a T-shirt, or album).

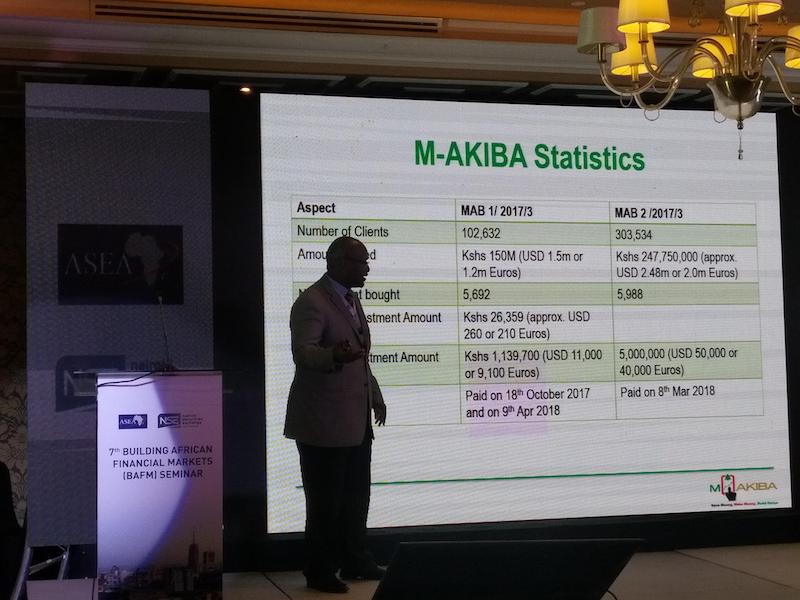

David Wagemma spoke about M-Akiba which was the first mobile-traded government bond in the world that cost Kenyan investors just $30 and which took five minutes to sign up and pay for, all via their mobile phones.

David Wagemma spoke about M-Akiba which was the first mobile-traded government bond in the world that cost Kenyan investors just $30 and which took five minutes to sign up and pay for, all via their mobile phones.

Later in a panel on block-chain as a disruptive technology for markets, Abubakar Mayanja said that progressive regulators should have sandbox licensing so that regulation goes on even as new ideas are developed, while Reggie Middleton, said the 1,500 cryptocurrencies in existence could grow on their own without needing each other and they did not need to concern central bankers and regulators in Africa as they had nothing to do with currencies.

In their remarks to close the event, Geoffrey Odundo, CEO of the Nairobi Securities Exchange (NSE), thanked organizers, saying that the BAFM had trended for two days and he saw that even the Deputy President was still following the conversation, while Oscar Onyema, President of African Securities Exchanges Association (ASEA) said that this had been the best event in the BAFM series, with the next one to be hosted by the BRVM in Ivory Coast in April 2019 – who would be challenged to excel of the Nairobi event

Day two of the 7th Building African Financial Markets seminar was held at the Villa Rosa Kempinski Hotel in Nairobi Kenya on April 20, 2018.