Edit September 2018: Ogilvy Africa has opened a Nigeria office ahead of the celebration of its 70th anniversary. The opening of the 24th office in Sub-Saharan Africa comes after an out-of court-settlement that the firm reached with Prima Garnet Communications who previously represented Ogilvy in Nigeria.

July 2010: At the end of April Scangroup announced a deal to buy into the Ogilvy Africa group and has now invited its shareholders to approve the transactions.

1. The acquisition of 51% in O&M Africa and 50% in Ogilvy East Africa will be structured as

- O&M Africa: 51% is to be acquired by payment of $238,360 (Kshs 19 million) cash and transfer of 6.2 million shares of Scangroup worth Kshs 166 million.

- Ogilvy East Africa: 50% will be acquired by payment of Kshs 13 million to Ogilvy South Africa (paid in US$) and transfer 4.4 million shares worth Kshs 118 million, and a payment to fellow shareholder Russell Holding of one euro and payments to Koome Mwambia comprising cash of Kshs 20.6 million and transfer of 3.12 million Scangroup shares worth Kshs 82.4 million.

2. Shareholders will have to approve the creation of 14 million new shares and waive their pre-emptive rights to allow the new shares to be allotted to Ogilvy South Africa and Koome Mwambia.

Winners

- Scangroup gains entry via minority shareholding in Ogilvy into Namibia, Cote d’Ivoire, Senegal, Burkina Faso, Cameroon, Gabon, Zimbabwe, Nigeria and non-equity affiliates in 11 other African countries to create a Pan-African agency.

- Koome Mwambia sells out his shareholding gets cash and becomes a top 10 shareholder in Scangroup and he is to enter into a management agreement to remain MD Ogilvy East Africa.

- MD Bharat Thakrar gains a pan African footprint and loses just 5%.

Losers

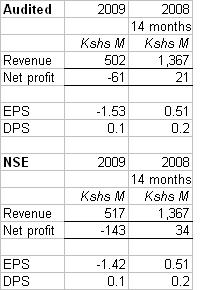

- Local investment bankers: No transaction advisers were appointed and the IM only has an opinion from BDO East Africa that the issue price of Kshs 26.4 is fair and reasonable and that Deloitte’s calculation of this price (Scangroup now trades at Kshs 36).

- Kenyan corporates whose choice of partners in media, PR, advertising got smaller – as Scangroup, Ogilvy, Hill & Knowlton, Blueprint, Mindshare, Millard Brown, Squad Digital, Smollan are all under one roof.

- Scangroup if the share swaps are denied by the South African authorities, will have to pay Kshs 427 million ($5.2 million) to proceed.