one of three

Over the last few years’ shareholders have voted to allow their companies to reproduce abridged financial statement summaries in the newspaper. One of the benefits of these resolutions would be to reduce costs of administering to thousands of shareholder, who previously were entitled to receive a full copy of a company’s audited results by mail.

Now companies have the full accounts on their websites for shareholders, to download, with a summary of the annual general meeting notice, dividend, chairman statement, and financial summary that appear in daily newspapers.

Limited numbers of the accounts are still printed and kept at the company premises, and distributed to analysts, partners, or to any shareholder who requests one. However most shareholders do not have Internet access or computers to read these PDF’s and may miss out on some details of events at the company.

Three companies are about to have their annual general meetings in the next few days, and have all converted to the digital format in lieu of printed copies. Kenya Airways and Safaricom both had their financial year-end in March 2010, while Access Kenya has had a good year (2009), but their meeting was delayed by boardroom wrangles which saw a new chairman brought in, and later by a drop in first half 2010 results (announced earlier this month).

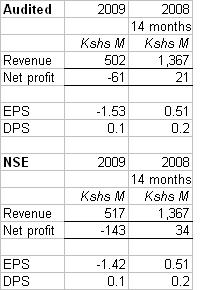

AGM – Auditors Deloitte continue in office (new Chairman Mr. Ndonye was a long time partner there)

– Shareholders will be asked to endorse a concluded deal to buy out the remaining 30% in Openview, which they describe as a company that sells IT equipment to enterprises and corporate customers. Openview had sales in 2009 of 165 million, up from 147m the year before, but it seems the minority owners opted to sell the company to AK (their right under original sale agreement), and a settlement was reached where payment was made by share transfers, but they also agreed to pay Kshs 38 million to settle some claims by AK group

Notes – Dividend of 0.3 shillings per share will be paid for 2009, amounting to about Kshs 62 million

– AK still enjoys benefit of listing as a group by paying 20% in income tax compared to subsidiaries and other Kenyan corporates, which pay 30%

– Borrowings are up to 724 million (57m in 2009), but overdraft has been reduced from 166 million to 30 million. The group still has an overdraft position of 128 million. The loans are from NIC Bank and CFC Stanbic for both US$ and KES, with the bulk of this borrowing is in US$ which is cheaper (3%) is cheaper than the shillings ones (7%), unless the shilling depreciated significantly. Interest expenses for the year were 44 million compared to 6 million in 2008

– Communications solutions limited charged 370 million as management fee and owes 364 million

– Fibre: AK paid 106 million as investment into TEAMS (62.5 shares)

Shareholders: Has 32,674 shareholders and while there are some top shareholder changes, the AK ESOP has increased stake in the company

Website AK has an active presence on twitter, but is hounded by claims of poor customer service. Also from Twitter: The board has indicated there is strong interest in acquiring the company from three Telco’s but Safaricom have denied being one of them

-@bankelele reading vacationing @alykhansatchu in the star – safaricom share dips back below IPO price as CEO denies interest in buying access kenya

– @jgmbugua MJ is lying. I have impeccable information that they have approached AccessKenya at least three times. TKL, Airtel interested too

– @coldtusker @jgmbugua @bankelele Maybe in the past but does #AccessKenya add real value to @SafaricomLtd today? [I say no]