Yesterday, Arsenal Holdings, parent of Arsenal Football Club held their annual general meeting (AGM) at Emirates Stadium, London. There were news reports about some tense moments and here a full recap of the AGM

Here’s a peek at their latest 67-page annual report (PDF) for the year ended, 31 May 2017.

For 2017, Arsenal income was £432 million (up from £353M the year before) and this comprised £100 million from match day revenue (26 home games had average ticket sales of 59,886 attendees), £198M from broadcasting, £90M from ‘commercial’, £26M from retail and £7M from player trading.

Group profit before tax was £44M in 2017 up from £3M and the tax charge for the year was £9 million up from £1.2M. This was at a tax rate of 19.86% and this will go down to 17% from April 2020.

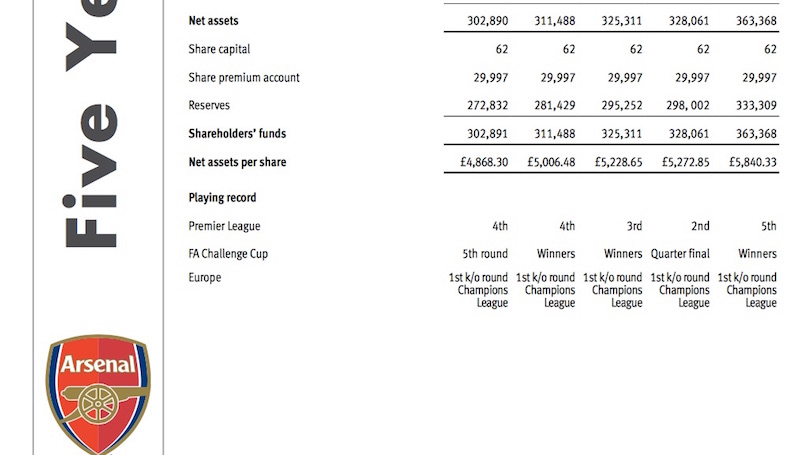

Arsenal Assets and Achievements in the last 5 years.

Over five years, turnover has gone from £280M to £424M and profit after tax from £4.9 million to £35.2M. Over the same period, net assets have gone from £302M to £363 M and fixed assets are now £618M (up from £572M in 2016)

Operating expenses were £371M including £199 million on staff, £79M on other, expenses and £77M on amortization of players, (the increased amortization charge is a direct result of a record level of investment into the Club’s playing resources). Led by the acquisitions of Granit Xhaka, Shkodran Mustafi and Lucas Perez the Club invested £113.9 million in acquiring new players and to a lesser extent extending the contracts of certain existing players, for example Hector Bellerin).

Arsenal staff payments totaled £199M in 2017 to 695 employees who comprised 75 players, 117 training staff (the development of our own players through our academy remains a priority for our football club), 395 administration staff and 112 ground staff.

In 2017 Arsenal paid £111M for players compared to £66M the year before and received £9M (compared to £12M in 2016). The Club was fully compliant with the Premier League’s wage cap/short-term cost control regulations – The ratio of total wage bill to football revenues was reduced to 47.2% (2016 – 55.7%).

Arsenal directors earned £25,000 per year, but the total payment to directors was £3M with I. Gazidis (CEO – £2.6 million) and K. J. Friar (Club Managing Director – £664,000) earning the bulk, as one director, Lord Harris of Peckham, waived his director’s fee and donated it to charity. The accounts were audited by Deloitte who also earned £25,000 for this report.

The report lists highlight of the year; how they did in tournaments, a win percentage of 63% (up from 52%,) and names individual players, goal scorers, and some transfers (we secured Sead Kolasinac and Alexandre Lacazette, our two primary targets for this transfer window)

Risks: These include the adverse impact of competing in the UEFA Europa League (they missed out on the 2017/18 Champion league), which is forecast to be £20 million. The full financial impact will depend on a number of factors including the actual progress made in the competition, as this impacts both performance and market pool distributions from UEFA. The Club has previously fully self-insured against a season’s participation in the UEFA Europa League within its cash reserves. Another risk highlighted in the annual report is from BREXIT – the Group is monitoring the impact of the UK’s decision to leave the European Union. This weaker pound against the Euro has already made it more costly for them to get players from the European Union, but that the greatest risk is from an economic downtown in Britain which will affect their revenue from broadcasting and sponsorships.

Finances: Arsenal has approximately £200 million of debt most of which is long-term and which mature in over 5 years. For 2017, the fixed bonds were at 5.8% and the floating ones at 7.0%. As part of its bond covenants, Arsenal has to maintain a certain amount of cash in the bank – and had £103 million in 2017 (compared to £117 million in 2016). They owe £47 million from recent player transfers. Finance charges in the year were £14M, which included bond repayments of £11M. Arsenal has exposure to the Euro and the US dollar on currencies and uses interest rate swaps for its bonds.

Subsidiaries & Investments: The Arsenal group has about 20 subsidiaries in which they own 100% of and which are used to manage areas like property development, retail operations, ladies football, stadium operations, and data management. Arsenal has also invested £20 million in a company that runs the club’s portal – Arsenal.com has 25 million unique visits a year; the club has 10 million Twitter followers with 9.6 million others on Instagram.

Partnerships: Their main partnerships are with Puma and Emirates. During the year, there was an increase in commercial revenues of £10.3 million, driven primarily by secondary partnerships. There’s no mention of deals in Kenya, which may include Sportpesa and Wadi Degla.

Edit: On November 17, Arsenal welcomed WorldRemit as its first-ever official online money transfer partner. The partnership will support WorldRemit’s growth ambitions by helping them reach Arsenal’s 74 million followers on their official social media channels and 185 supporters’ clubs worldwide.

For Investors:

- Over a five-year period, earnings per share have gone from £78 to £567 per share. There are 62,217 shares issued.

- The ultimate parent of Arsenal is KSE UK (which owns 67.05%) which is wholly-owned and controlled by E.S. Kroenke.

- The directors do not recommend the payment of a dividend for the year (2016 – £Nil).

- See this on buying shares in Arsenal football club.