Some are carry-overs from 2015, but still having an impact on the banking sector in 2016 include:

1. The shutdown of Chase Bank in April 2016 came after a 24-hour period that started with a second set of 2014 financial accounts published in unclear circumstances in a newspaper, with different figures. Whether this was due to a reclassification of Shariah loans or (insider) director lending was never explained, but it accelerated an ongoing run of withdrawals and the Central Bank had to close the bank the next day. While it reopened a few weeks later with funding from the central bank (channeled through KCB), and depositors have been able to access some of their funds, the bank is not back to its full standing (it’s till not lending in full, and there’s a moratorium on depositors interest) and new investors are being sought to enable the bank to stand on its own from April 2017.

2 Njomo Bill: In a rare bi-partisan move, usually reserved for their own salary raises, members of parliament rallied around to take on an even less popular target – that of super profit making, high-interest rate, banks with the Njomo bill. This was the latest attempt to rein in interest rates and the president surprisingly signed the bill, passing on a hot potato which was expected to lead to a slowdown in lending and make banks less attractive to investors.

3. Governor Patrick Njoroge at the Central Bank. Widely admired by the public for his no-nonsense enforcement & understanding of rules, supervision, austerity, and honestly to clean up the banking sector, but vilified in some circles for his unreasonable decision-making that has seen three banks close under his watch.

4. Last year Imperial Bank closure was a shock, and in 2016 the extent of the shell is still becoming clear through numerous court documents pitting the receivers, regulators, shareholders, some customers and even the family of the later managing director who engineered the fraud. But all that pained depositors want to know is, where is the money, how much money is there, and when will they get paid?

5. Lax government banking. From not following up whistleblowers on Family, Chase and Imperial, to a reluctance to act on South Sudan leaders. From double payments to government contractors, to county and national governments having dozens of banks accounts for inexplicable reasons. From a parastatal moving to a single signatory and withdrawing all its’ funds to pay a fictitious contract, and the funny banking of NYS money by Josephine Kabura at Family Bank. The anti-fraud / anti-money laundering/ anti-terror rules are not being observed.

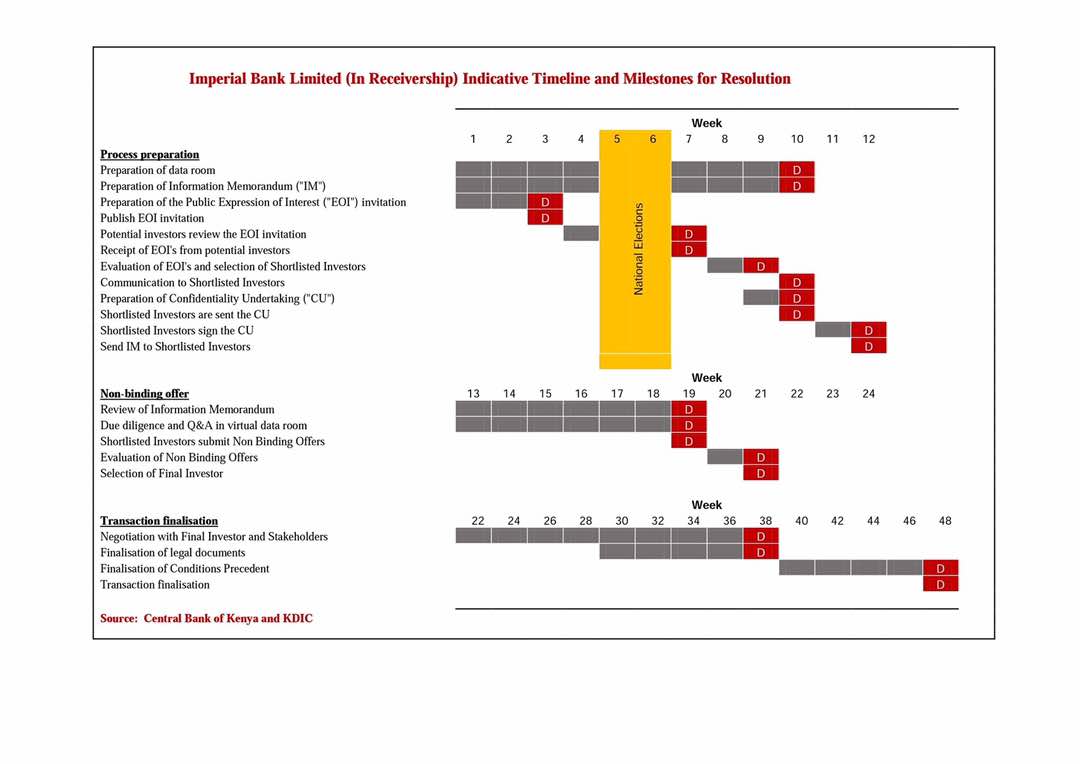

Now, the envisioned recovery process is similar to one being used for Chase Bank which is open, but still in receivership. Expressions of interest are invited from strategic investors. They will be evaluated and the short-listed ones will be given further confidential data to enable them to do due diligence and come up with formal offers that they will present to the to the receiver-manager to decide on. The process will take about a year.

Now, the envisioned recovery process is similar to one being used for Chase Bank which is open, but still in receivership. Expressions of interest are invited from strategic investors. They will be evaluated and the short-listed ones will be given further confidential data to enable them to do due diligence and come up with formal offers that they will present to the to the receiver-manager to decide on. The process will take about a year.