A guest post by Michael Kimani (@pesa_africa)

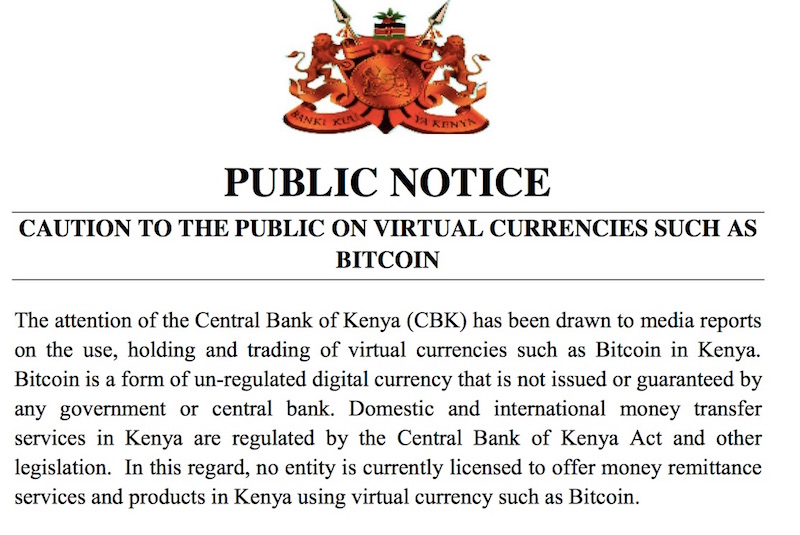

On Tuesday, December 15th , the Central Bank of Kenya issued a public notice on bitcoin in the Daily Nation: CAUTION TO THE PUBLIC ON VIRTUAL CURRENCIES SUCH AS BITCOIN – it read. Naturally, as an analyst keen on this space, I had been expecting this. As part of the Bitcoin community here in Kenya, I am a vocal advocate of digital currencies, writing extensively on the subject over the past 2 years. Suffice to say, I have a firm grasp of Bitcoin in whole. CBK assertions were wide off the mark, and I cannot help but question the competency of their research. With this Op Ed, I shall clarify the downright falsehoods in its notice.

Right of the bat, the headline ‘caution on Virtual currencies such as Bitcoin’ is not well thought out. Virtual currencies is a broad term encompassing reward schemes we use in Kenya today – Bonga, Nakumatt, Uchumi points and Kenya Airways (KQ frequent flyer) points. According to the European Central bank, they are ‘digital representations of value not issued by government that can be used for payments.’ Evidently, Bitcoin and bonga points fall in the same category. As such, they should be treated in the same manner, as there is no explicit regulation for virtual currencies in Kenya.

Bitcoin has a unique design, that confounds regulators and monetary authorities attempting to pigeonhole it. It is by no means legal tender in Kenya, nor anywhere else, consequently, its legal status varies substantially from country to country.

For example, US tax authority IRS classifies it as an asset, with tax payable on capital gains. Across the European Union, bitcoin is treated as a means of payment, after a top court ruling in October exempted it from VAT, just like regular cash. On the contrary, a ruling by US Commodities Futures Trading Commission (CFTC) in September, officially defined it as a commodity, just like wheat and crude oil. The UK, considers it as private money and sales of goods and service in exchange for bitcoin are subject to VAT.

Under the hood, bitcoin is an artificially scarce economic incentive for securing a decentralized ‘internet like’ network – the first of its kind. One popular application for it right now, is an open source global payment network but, that is just the tip of the iceberg. You see, the network, referred to as the blockchain in tech circles, is also a platform for building all sorts of fascinating applications never before possible. All are joined at the hip. No wonder, governments and legal experts have trouble confining it. Meanwhile, Silicon Valley hails it as the greatest innovation in the past 100 years – the internet of money.

Reading on, CBK highlights three risks associated with bitcoin –

- ‘bitcoin transactions are largely untraceable and anonymous making them susceptible to abuse. . .’ All too often, I come across this fallacy, regurgitated by uninitiated commentators. For the record, Bitcoin transactions are visible on a public ledger that holds a permanent record of all transactions since inception. Transactions are traceable and pseudonymous, so much so, that the UK treasury, deemed it low risk for money laundering and terrorism financing in a National Risk Assessment report released in October, 2015. Notably, the UK has taken measures to embrace bitcoin and digital currencies as a strategic competitive advantage; Kenya would do well to take a leaf out of their book.

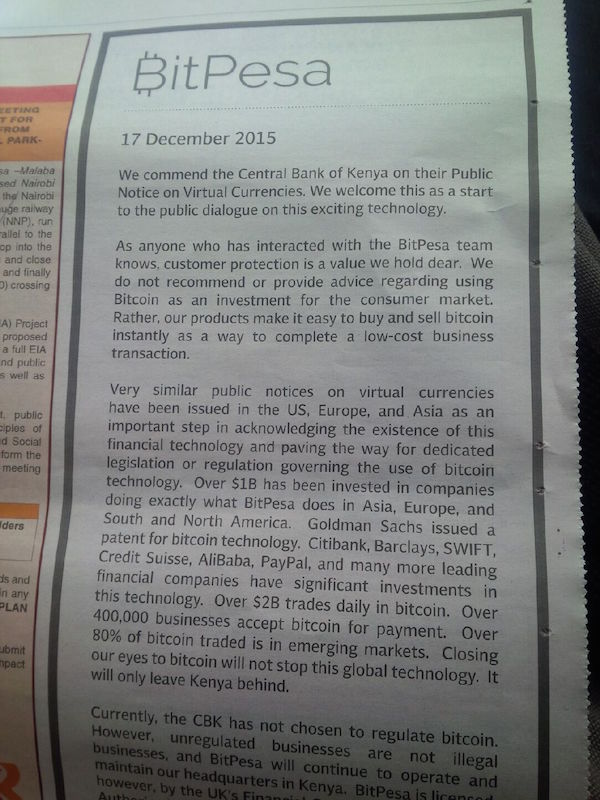

- “Virtual currencies are traded in exchange platforms that tend to be unregulated all over the world” While this may have been true 2 years ago, it is no longer the case. Regulation around the world has caught up, bridging the gap between mainstream investors and bitcoin. Bitcoin Investment Trust is a US bitcoin investment vehicle trading on OTCQX, the most heavily regulated of over-the-counter exchanges. In Sweden, investors can buy Bitcoin via an exchange-traded note (ETN) listed on Nasdaq Stockholm stock exchange. Coinbase and itBit are regulated bitcoin exchanges in the United States. Gone are the sloppy days of Mt. Gox, exchange platforms today are run by professionals. Additionally, in Kenya, purchased bitcoins remain in full control of their owners, at all times. As a digital bearer asset, holders have the keys to their coins, therefore, if BitPesa ‘collapsed or close business’ today, no single user would lose access to their bitcoins.

- Finally, bitcoin is indeed volatile, as its value fluctuates based on free market forces. There is no Central Bank to step in with monetary policy, because it is not issued by a central authority. In fact, this design was intended from the beginning. Uniquely, its monetary base supply is capped at 21 million bitcoins, a fact that drives speculative interest, expecting its deflationary nature to ramp up its price up over time. In 2009, 1 bitcoin was trading at $ 0.001, by November 2013, price was up to $ 1,173; as of writing this, it is just above $450. I would not recommend it to anyone who was not fully aware of the risk reward ratio.

There is a lot more to bitcoin than could fit this post. My advice is to conduct your own research and due diligence, you will find it fascinating at the very the least. I am confident bitcoin and the blockchain will come out on top as the greatest innovation of our time. Four years from now, we will look back and laugh at how ridiculous this notice was.