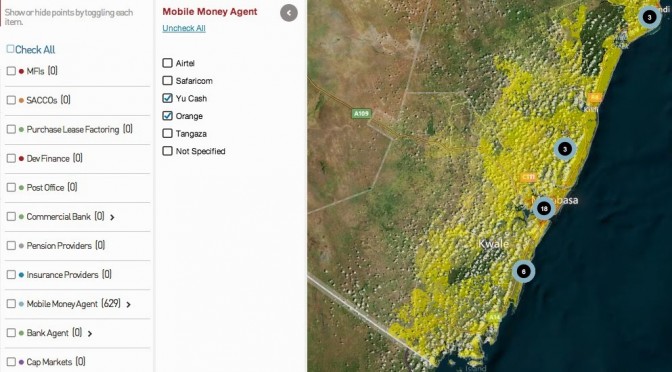

This week, FSD Kenya launched an interactive tool called the FinAccess Spatial Map that mapped all the formal financial service points in Kenya. This has been an ongoing private-public partnership, and it’s notable as a previous FSD study on the numbers of ‘unbanked’ Kenyans became the justification for the relatively unregulated roll out of m-pesa and mobile money in the country.

The searchable tool interprets data like financial service points (GIS locations of bank branches, mobile money agent), county borders, and local population numbers from the census – to plot some interesting metrics.

The tool tends to find that there are more financial service points in wealthier parts of the country (no surprise) and that more Kenyans live closer to a mobile money point (58% are within 3 kilometers of one) than a bank branch (21%). It can also pick out useful trends for further research e.g. at the launch, it was mentioned that in Isiolo, 40% of the population own mobile phones, but only 20% use mobile money, while in Nyeri, 75% own phones, but an even larger number – 80% use mobile money.

Partners in the FSD mapping program included the Central Bank of Kenya, Brand Fusion, SpatialDev, and the Bill & Melinda Gates Foundation.